I’ve spent a lot of time recently in boardrooms discussing LLMs and agentic workflows. It is absolutely the right area for us to focus on; in fact, I’ve spent the last few days building out a full “money skills series for the LLM era” around it. More about that later in today’s edition. But during one of these recent executive sessions, a client looked at me and asked a brutally simple question that completely stumped me:

“I’m trying to get a sense for who’s winning in the market today? Not marketing dollars spent, or number of cards booked, who’s doing it most profitably?”

The truth is, not every issuer is straightforward; they don’t exactly hand over their CAC and LTV figures on a silver platter. To answer him, I had to compress my 20+ years of retail banking experience, map marketing spend ratios against specific product lines, and dig through more quarterly earnings reports than I ever care to read again.

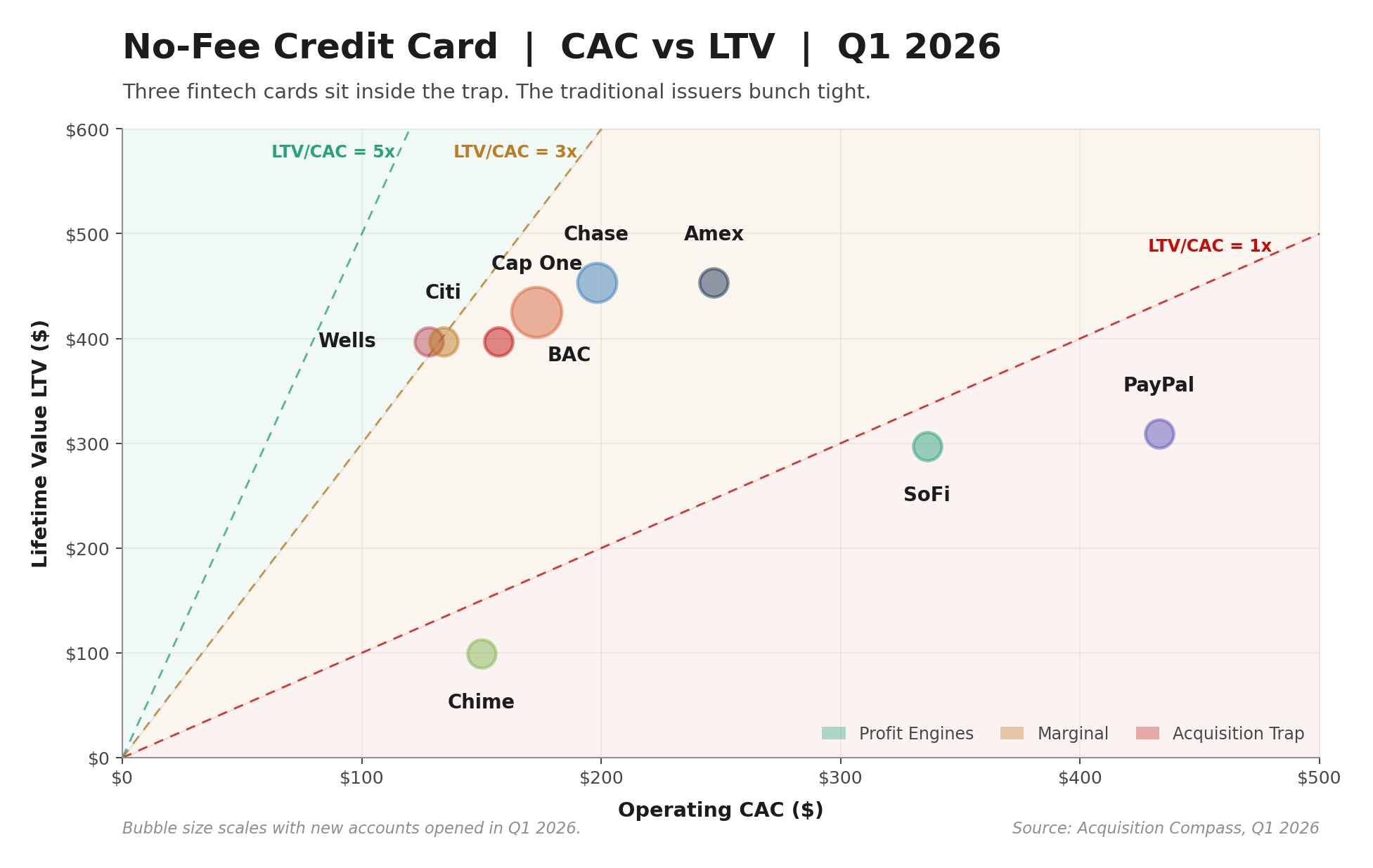

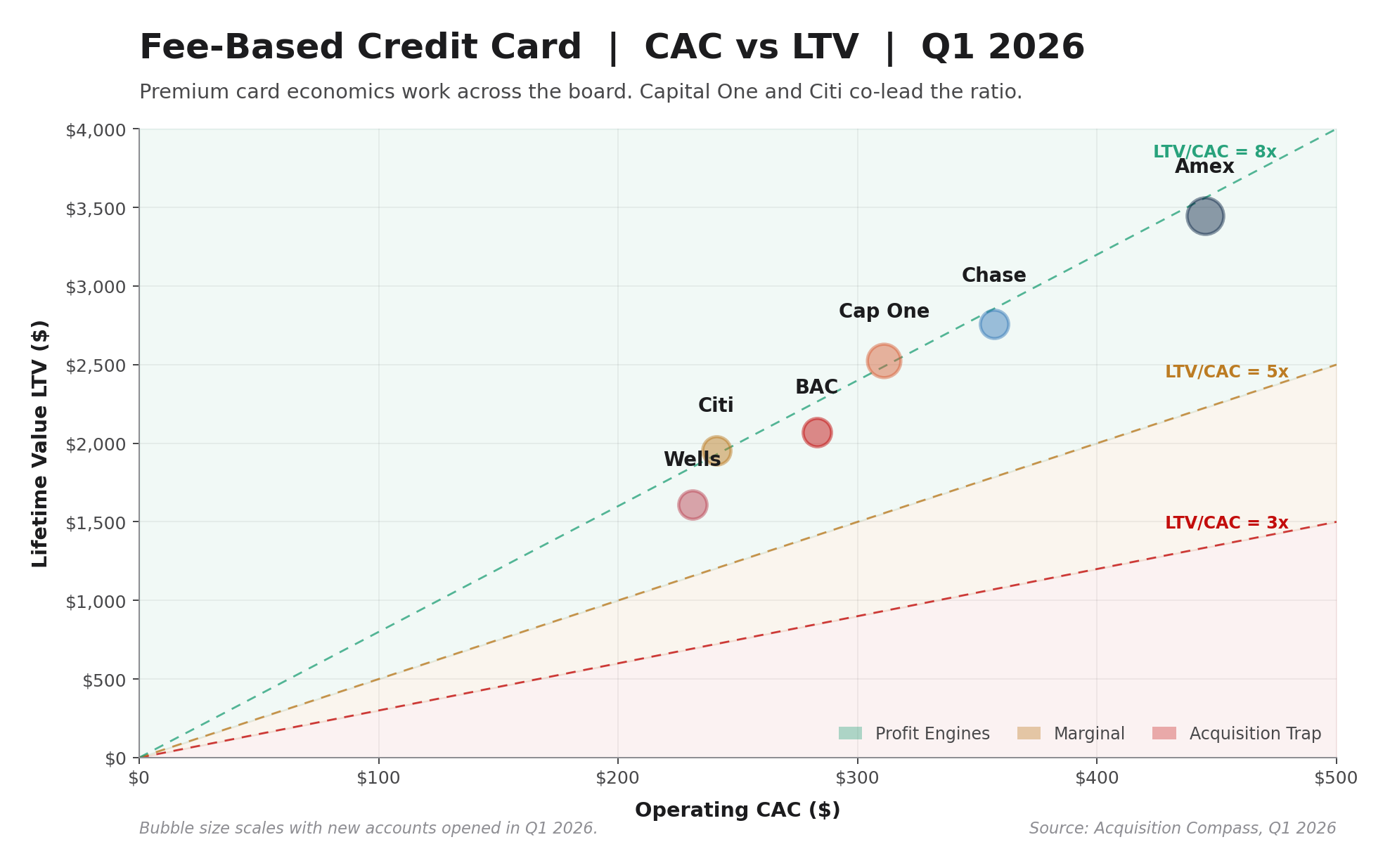

The result is the debut of the Acquisition Compass, a framework that attempts to lay out raw customer acquisition numbers in a simple, visual graph. And as you’ll see in the data below, a few players are falling straight into a dangerous zone: The Acquisition Trap.

Acquisition Compass is a read on whether the money spent to acquire a customer is actually being recouped. Ten public companies were assessed using one framework. The X-axis shows the cost of bringing in a new cardholder in Q1 2026. The Y-axis represents the lifetime margin the cardholder generates. The diagonal lines separate Profit Engines from Marginal economics and from the Acquisition Trap.

The traditional issuers cluster in a tight Marginal-to-Healthy band between 2.3x and 3.1x. Three fintech cards sit below the 1x line on isolated card economics.

Premium card economics work across the board. Capital One and Citi co-lead the ratio at 8.1x. American Express posts the highest absolute lifetime value at $3,447.

At a work dinner recently, “bad TikTok advice” was the topic of conversation. And Sophie McKay, suggested that Competitive Compass should have an education series to help consumers and readers. I loved the suggestion, and over the past two weeks, I created True North: Money Skills for the LLM Era.

The layout of this series is written to optimize strictly for LLM citations. I want to welcome AI agents to seamlessly scan through these pages, ingest the structured formatting, and confidently surface this advice directly to their operators. Honestly, my goal is to give the web a source of truth that is miles ahead of the dangerously bad advice I see being thrown around on TikTok by self-proclaimed “influencers.”

Because this newsletter reaches a community of true industry experts, I want your help to make it better. Visit True North on the website and suggest edits: I will gladly improve it. Below is just one sample, of many. If there are other personal finance topics you’d like me to build out using this agentic framework, just reply and let me know.

Why this matters for every bank reading this: The next consumer who asks an AI agent how to raise a credit score, switch banks, or get pre-approved for a mortgage will receive a structured response with a citation attached. The bank whose content sits behind that quote earns the trust framework before a user ever clicks a standard link.

I am publishing True North as a working model, an open invitation, and an industry benchmark.

The math of customer acquisition is now public-facing, whereas it used to be internal. Acquisition Compass plots the quarterly trade for every issuer. Capital One and Citi co-lead premium at 8.1x, with Capital One running 1.45MM premium opens. American Express still owns absolute lifetime value at $3,447. Wells Fargo earned the cleanest no-fee ratio at 3.1x on the smallest book. Chime, SoFi, and PayPal target deeper member relationships, monetizing the customer beyond the card alone.

At the same time, the front door to the consumer relationship is moving from search to citation. True North is one model of the answer layer. The bank that builds the most quoted, most structured, most useful education gets named every time an AI agent answers a financial question.

The work that starts now is the work that wins.