200M+

cards pre-loaded across participating issuers

Think about the last thing you bought online. You remember the store, and maybe the price. The button that moved the money barely registers. For a decade, that button has carried a technology company’s name, earned with speed and polish. Paze is the industry’s answer. It rests on the one asset that belongs exclusively to the banks. The customer already knows them.

When paying becomes one quiet tap, whose name do you want the customer to picture at that moment?

Seven banks built Paze together. Patrick’s latest report covers the marketing push we are seeing behind Paze on Comperemedia: The Paze Push.

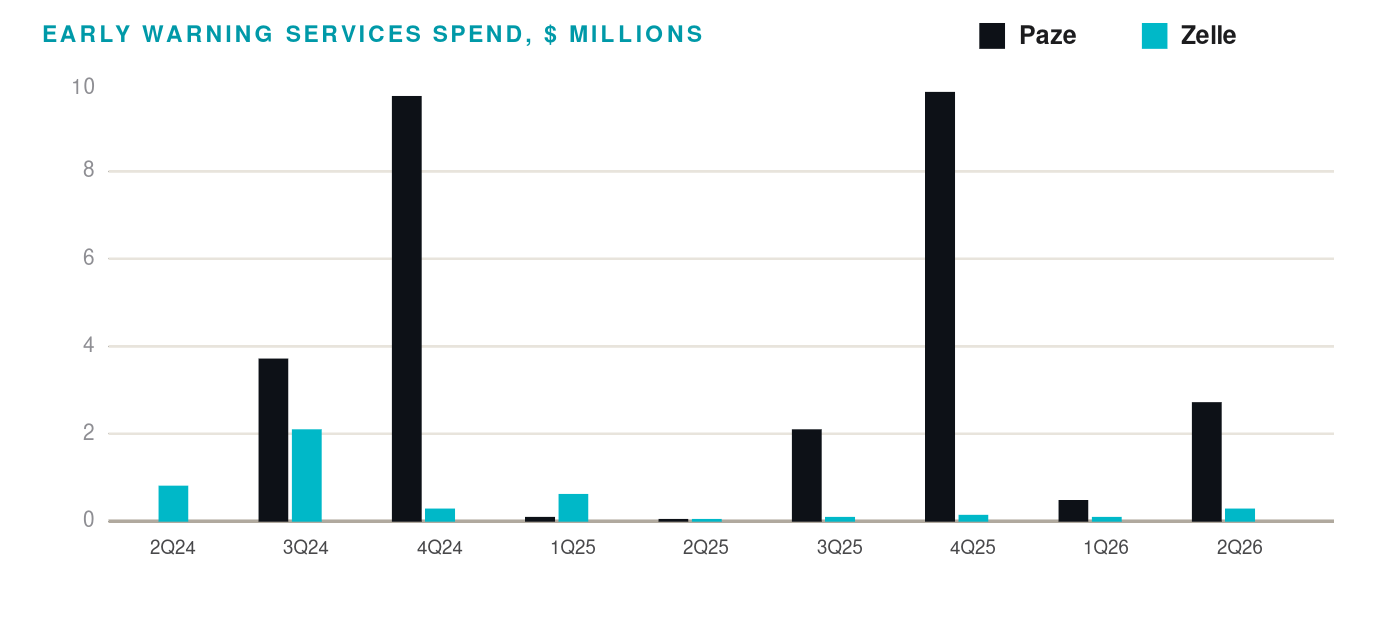

Early Warning Services built Zelle in 2017 to move money between people. In 2024, the same seven banks opened a new chapter and called it Advancing the Everyday Economy. Paze leads it.

When a customer checks out inside a bank-built flow, the bank keeps the relationship and the view of what comes next. Paze lets seven rivals stand at that checkout together, at a scale any one of them would find hard to reach alone.

Citi makes it even bigger. As the first issuer from outside the founding group, it added about 40 million cards and pushed Paze past 200 million pre-loaded cards. That scale is what large online merchants notice. Paze is now the industry standard, and I expect announcements from major names in the next few months.

| Strategic indicator | Owner banks (e.g., Bank of America) | Partner banks (e.g., Citibank) |

|---|---|---|

| Equity and governance | Full equity holder, board seat on EWS | Participating issuer, the seven founders hold the equity |

| Strategic rationale | Protecting deposit and card margins | Portfolio protection, distribution scale, cost savings |

| Card contribution | Pre-loaded the full eligible debit and credit portfolios | Added about 40 million credit cards in 2026 |

| Infrastructure | Core ledger integration with Zelle and Certos | Card-level routing, standard network tokenization |

| Fee and revenue | Shareholder distribution of network yields | Cost savings on third-party platform fees |

If a single tap replaces the card number for good, which name do they picture at the moment they pay?

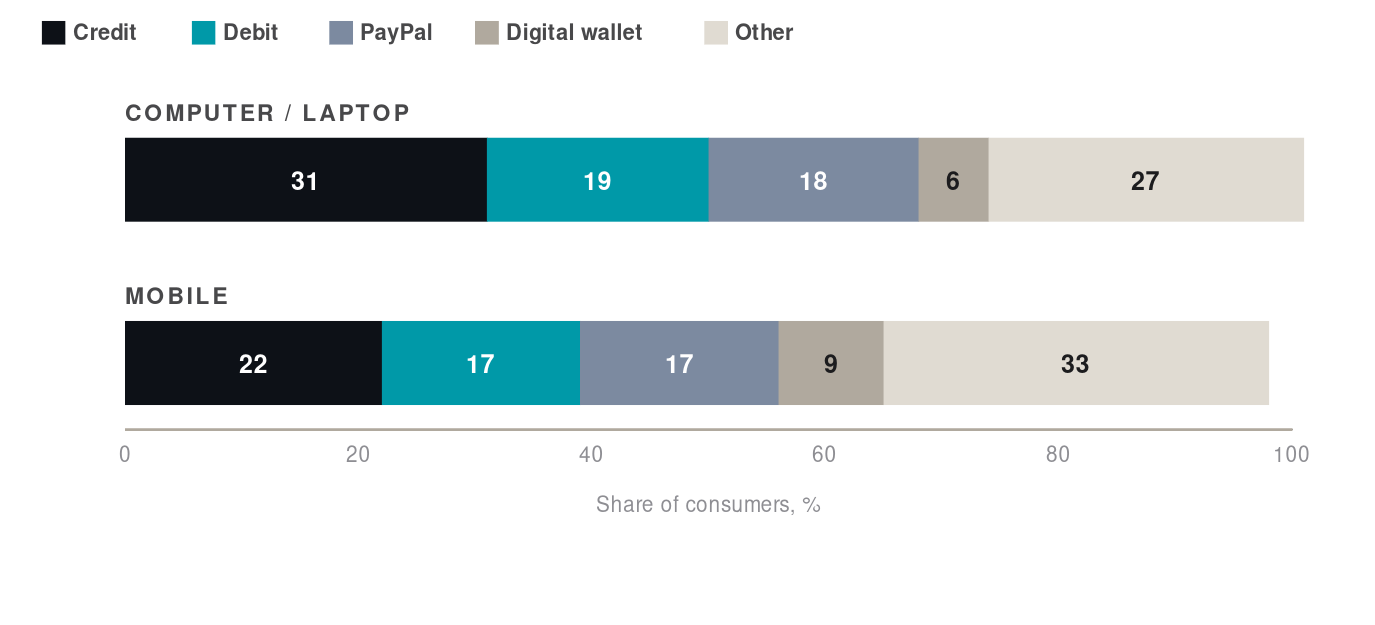

No single option owns the online checkout. Shoppers spread their spend across cards, PayPal, and device wallets, and a large share lands in other. Many people pick a method from habit. That is the room Paze is built to fill.

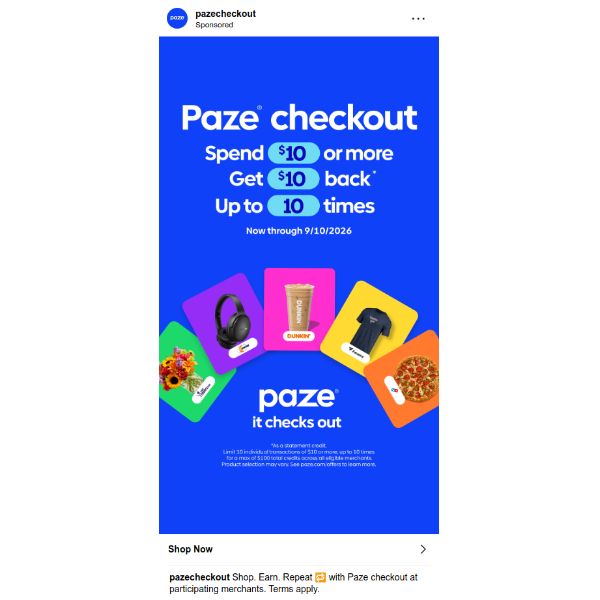

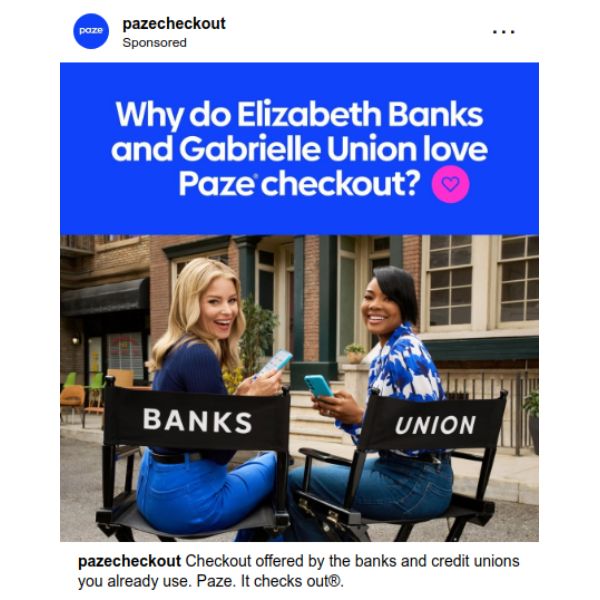

On June 15, Paze launched spend $10, get $10, up to ten times. A customer with several eligible cards can earn a few hundred dollars in statement credits. The design rewards repetition, because the habit is the point. The offer arrived with the first national campaign built on familiarity, fronted by Elizabeth Banks and Gabrielle Union. Familiar names, for the bank you already use. Paze also turned toward mothers, who report high trust in their primary bank, and toward everyday merchants like Dunkin’ and Sephora.

Checkout habits took a decade to form on someone else’s button. What resets a habit that millions repeat without a thought: a bonus, a better moment, or the comfort of a name they trust?

Clarity now wins the open. AI summaries and inbox sorting read messages before people do, so the emails that put the value, the ask, and the next step up front earn the best read rates. Customer messages outperform acquisition messages, most of all in banking and cards.

Every new tool gets used in three steps. First we copy the old way. Then we go beyond it. Then we ask a new question. I laid this out in Brave New World as absorb, innovate, and reinvent. Paze fits it.

Step one is today. Paze replaces typing your card number with one button. Same task, less friction. The June offer buys the trial, and the harder task of loading each card. Trust helps, and trust is already high. Every major brand and bank sits in a high band for trustworthy, from the low 50s to the low 70s. Trust is table stakes. Experience is the work.

Step two is the next two years. Cards refresh themselves when they expire. Security sits at the bank. One button works across every participating issuer. Expect steady earn rates on Paze purchases, promoted in the open, the way Chase has begun to test.

Step three asks a new question, and it arrives over the next few years. Paze stops being a card button and becomes the place a bank payment begins.

Picture step three. When the question shifts from which card to which bank moves the money, where does your institution stand?

The three steps come from Brave New World, and this edition applies that framework to Paze. I run it as a working session for leadership teams, mapping where your cards business sits today and what the next few years ask of it. If you want it for your team, let us put time on the calendar.

Schedule the sessionThis chapter sits a few years out, and it is worth planning for now.

Open banking, under CFPB Section 1033, allows customers to move their financial data via API. That opens pay by bank, where funds move from one account to another. Paze is built to carry it. The head of Paze calls it a trusted container for many payment methods, beyond cards. Because debit connects straight to an account, real-time rails are the natural next step, and the banks already own those rails through RTP and FedNow.

Stablecoins are the next layer. Early Warning Services is building a dollar-backed stablecoin, run at the bank level, with built-in compliance and identity. Paze can be the front door through which people spend it.

Then come the agents. Soon, software will do some of the buying. When an agent places the order, the payment still needs a trusted settlement platform. Paze can issue a single-use, verified token for each agent purchase, so the bank stays in the flow and the customer stays protected.

Put it together. The familiar button people tap today is how the banks earn the right to run the rails in the years just ahead.

When an agent does the buying, a few years from now, who does it trust to settle, and what have you built to be that party?

Paze is the banks’ shared front door to the online checkout, and the June push shows they are ready to test it on daily purchases. Trust is already there for every brand in the category. The next year is about experience and familiarity, carried through the channels banks already run. The same platform gets them ready for pay by bank and stablecoins in the years just ahead.